40 duration zero coupon bond

Macaulay Duration Zero Coupon Bond - RAEE Other factors include coupon rate and frequency, bond yield and any call features written into the bond. Like maturity, duration is also expressed in years. Note that any bond with a non-zero coupon will have a duration shorter than its maturity. For example, a 30 year bond with a 7% coupon and a 6% YTM has a duration of only 14.2 years ... PDF Duration - New York University Duration 7 For zero-coupon bonds, there is an explicit formula relating the zero price to the zero rate. We use this price-rate formula to get a formula for dollar duration. Of course, with a zero, the ability to approximate price change is not so important, because it's easy to do the exact calculation.

Modified duration of zero-coupond bond (FRM practice ... A zero-coupon bond with maturity of ten (10) years has a 6% bond-equivalent yield (semi-annual compounding). What is the bond's modified duration?

Duration zero coupon bond

Bond Yield to Maturity (YTM) Calculator - DQYDJ Yield to Maturity of Zero Coupon Bonds. A zero coupon bond is a bond which doesn't pay periodic payments, instead having only a face value (value at maturity) and a present value (current value). This makes calculating the yield to maturity of … The Macaulay Duration of a Zero-Coupon Bond in Excel Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and... The Macaulay Duration of a Zero-Coupon Bond in Excel ... Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and B, right-click on the columns, select "Column Width", and change the value to 30 for both columns.

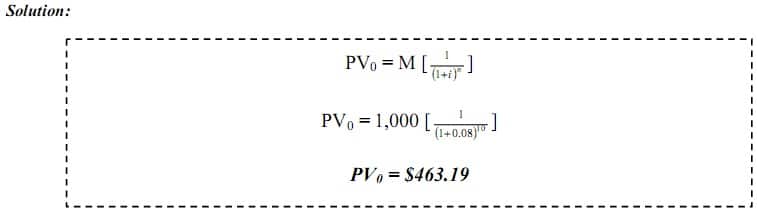

Duration zero coupon bond. Zero Coupon Bond (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. How Bond Maturity Works | Bonds | US News Mar 12, 2020 · A savings bond is an example of a zero-coupon bond because the interest payments are added to the bond's principal value, rather than paid out periodically. Holders can check savings bond maturity ... Short-Term ETF List - ETFdb.com Short-Term and all other bond durations are ranked based on their aggregate 3-month fund flows for all U.S.-listed bond ETFs that are classified by ETF Database as being mostly exposed to those respective bond durations. 3-month fund flows is a metric that can be used to gauge the perceived popularity amongst investors of Short-Term relative to ... Solved What will be the duration of a zero coupon bond ... What will be the duration of a zero coupon bond maturing in 5 years. Would the duration of the zero coupon bond be lower or higher than that of a 10% coupon bond maturing in 5 years. Provide a brief reasoning. Expert Answer 100% (1 rating) ANSWER - Duration of Zero coupon bond (ZCB) is the maturity time of the bond is 5 years.

What Is Bond Immunization? - Morningstar, Inc. You can buy one zero-coupon bond that will mature in five years to equal $50,000, or several coupon bonds each with a five year duration, or several bonds that "average" a five-year duration. Maturity Range Avg. Maturity Duration Yield to Worst TEY ... Municipal Bond Investor Weekly High Net Worth Wealth Solutions and Market Strategies // Fixed Income Solutions CAMILLE HERNANDEZ Director ... Maturity Range Avg. Maturity Duration Yield to Worst TEY* 1 to 5 3.0 2.78 2.27% 3.83% 5 to … Macaulay's Duration | Formula | Example Duration of Bond A is 4.5, i.e. the maturity period (in years) of the zero-coupon bond. Duration of Bond B is calculated by first finding the present value of each of the annual coupons and maturity value. Annual coupon is $50 (i.e. 5% of the $1,000) and the maturity value is $1,000. PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Modified Duration - Zero Coupon Bond Modified Duration ... We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%. The duration of a zero coupon bond is equal to the ... The duration of a zero coupon bond is equal to the The duration of a zero-coupon bond is equal to the maturity of that bond. For example, suppose we have a zero-coupon bond with 2 years to maturity trading at a YTM of 25%. If you calculate the duration you will find that it will be equal to two years. 3.7.4. Duration of an irredeemable bond. Duration: Understanding the Relationship Between Bond ... Duration is expressed in terms of years, but it is not the same thing as a bond's maturity date. That said, the maturity date of a bond is one of the key components in figuring duration, as is the bond's coupon rate. In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. Solved If the US Treasury issued a 5-year zero-coupon bond ... If the US Treasury issued a 5-year zero-coupon bond, what is its duration? *Put answer in excel sheet. Question: If the US Treasury issued a 5-year zero-coupon bond, what is its duration? *Put answer in excel sheet.

PPT - Duration and convexity for Fixed-Income Securities PowerPoint Presentation - ID:6690660

Macaulay Duration - Overview, How To Calculate, Factors A zero-coupon bond assumes the highest Macaulay duration compared with coupon bonds, assuming other features are the same. It is equal to the maturity for a zero-coupon bond and is less than the maturity for coupon bonds. Macaulay duration also demonstrates an inverse relationship with yield to maturity.

PPT - International Bond Market PowerPoint Presentation, free download - ID:1716507

Zero-coupon bond - Wikipedia A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years. For some Canadian bonds, the maturity may be over 90 years.

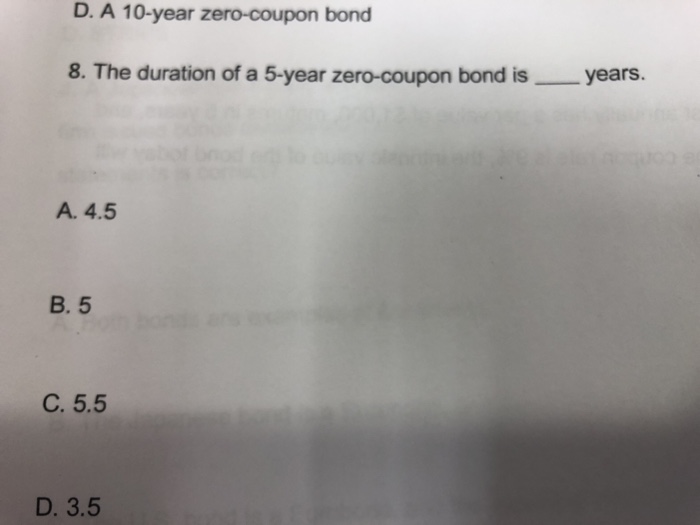

Solved: D. A 10-year Zero-coupon Bond 8. The Duration Of A... | Chegg.com

fixed income - Duration of callable zero coupon bond ... A 10-year zero coupon bond is callable annually at par (its face value) starting at the beginning of year 6. Assume a flat yield curve of 10%. What is the bond duration? A- 10 Years B- 5 Years C- 7.5 Years D- Cannot be determined based on the data given. According to me it should be 10 years as the duration of a zero coupon bond is always equal ...

On The Plotting of Yields

Bond Duration Calculator - Macaulay and Modified Duration ... Bond duration is a linear estimate of a bond's price sensitivity to changes in market yield. It's the first derivative of price with respect to market yield. However - the relationship between yield and price isn't linear, it's a curve. Bond convexity is the second derivative, and a measure of the "curvedness" of the relationship.

Bond 3

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Journal Entry for Zero Coupon Bonds | Accounting Education

Zero Coupon Bond Value Calculator: Calculate Price, Yield ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

Bond Discounting I Types I Examples I Formula I Bonds Valuation

DV01 (Dollar Duration) - WallStreetMojo DV01 simple calculation assumes that Bonds pay fixed coupon payments at regular intervals; however, there are certain categories of Bonds such as Floating Rate Bonds, Zero Coupon Bonds Zero Coupon Bonds In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued ...

Zero-coupon bond - PrepNuggets

What is the duration of a zero coupon bond? - Quora Originally Answered: what is the duration of a zero coupon bond? Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

Finding YTM of a Zero Coupon Bond (6.2.1) - YouTube

Zero Coupon Bond Calculator - MiniWebtool Zero Coupon Bond Definition A zero-coupon bond is a bond bought at a price lower than its face value, with the face value repaid at the time of maturity. It does not make periodic interest payments. When the bond reaches maturity, its investor receives its face value. It is also called a discount bond or deep discount bond. Formula

Solved: 25. A Zero Coupon Bond Refers To A Bond Which: Doe... | Chegg.com

Solved Given the time to maturity, the duration of a ... See the answer Given the time to maturity, the duration of a zero-coupon bond is a higher when the discount rate is _____ A.Higher B. Lower C. The bond's duration is independent of the discount rate D.None of the options are correct Expert Answer 100% (1 rating) Answer C. The bond's duration is independent of the discount rate. Bond dur …

zero-coupon bond | zero-coupon bond on board. You are allowe… | Flickr

Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

What is a Zero-Coupon Bond? Definition and Meaning - Market Business News

What Is Duration Of A Bond? - LudoPrevención One drawback to zero-coupon bonds is their pricing sensitivity based on the prevailing market interest rate conditions. If the market yield increases by 1% the bond's price will decrease by $60. what is the duration of a zero coupon bond If the market yield decreases by 1% the bond's price will increase by $60. Sign Up For Investor Updates

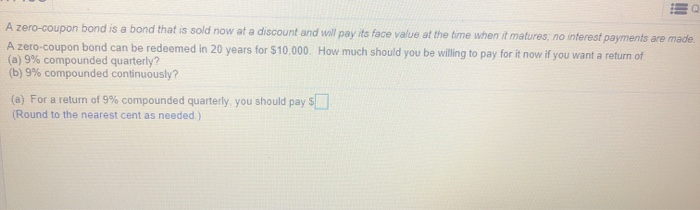

Solved: A Zero-coupon Bond Is A Bond That Is Sold Now At A... | Chegg.com

PDF Bonds - Wharton Finance Zero Coupon Bonds zWhy do zero-coupon bond prices change?...Interest rates change! zThe price of a zero-coupon bond maturing in one year from today with face value $100 and an APR of 10% is: zExample: Now imagine that immediately after you buy the bond, the interest rate increase to 15%. What is the price of the bond now 0 ()1 N F V i = + 0 ()1 ...

Duration of a Bond | Portfolio Duration | Macaulay & Modified Duration

duration of zero coupon bonds | Forum | Bionic Turtle The Macaulay duration of a zero-coupon bond equals its maturity, such that the Mac duration of a zero-coupon bond must be monotonically increasing, and. DV01 = Price * Mod duration /10000, where in the case of a zero coupon bond: Price is a decreasing function of maturity (i.e., a zero is acutely "pulled to par"), but Mod duration is an ...

Solved: You Find A Zero Coupon Bond With A Par Value Of $1... | Chegg.com

PDF APPENDIX 3A: Duration and Immunization maturity and duration zero-coupon bond or a coupon bond with a five-year duration, the FI would produce a $1,469 cash flow in five years, no matter what happens to interest rates in the immediate future. Next we consider the two strategies: buying five-year deep-discount bonds and buying five-year duration coupon bonds.

Ppt

Zero Coupon Bond Calculator - What is the Market Price ... Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) Zero coupon bonds are particularly sensitive to interest rates, so they are also sensitive to inflation risks. Inflation both erodes the ...

Post a Comment for "40 duration zero coupon bond"